WEEKLY MARKET ANALYSIS BY MANOKARAN MOTTAIN

THE benchmark KLCI Index ended the holiday shortened trading week on a higher note at 1,431.04 points (+15.09 points or +1.06%).

However, it was achieved on thin trading volume as the average daily value remained roughly similar to the previous week at RM1.51 billion per day from RM1.54 billion per day last week. Last week’s trading value was 24% below the past 100-day average daily trading value of RM1.99 billion per day.

In the bond market, US bond yields has started consolidating after the US Federal Reserve raised the Federal Funds Rate for the 10th consecutive time to a target range of between 5.00% to 5.25% (the highest since August 2007) and indicated that this could be the final rate hike after removing comments on additional policy firming in the post meeting statement.

This means that future policy decisions would be data dependent. However, US Federal Reserve Chairman said there will be a long time before inflation goes back to its 2% target and interest rate cuts may be a long time off.

Meanwhile, the Bureau of Labour Statistics disclosed that the US economy added 253,000 non-farm payrolls in April 2023, far ahead of the 180,000 jobs expected by economists. The unemployment rate of 3.4% was also much lower than the 3.6% estimated by consensus.

A strong and robust jobs market supports the view that the Federal Reserve will not be pivoting its interest rate trajectory as fast as the market expects.

The bond markets was also calmed by news that JP Morgan Chase took over First Republic Bank (FRB) after regulators seized First Republic and put it for sale. A last minute effort by the management of FRB to keep the ailing bank afloat failed after its clients withdrew more than US$100 billion in deposits. This was the third bank failure in the US since March this year.

The 10-year US Treasury (UST) yields remained steady as it fell by just a single (1) basis point to 3.44% from 3.45% in the previous week and further reduced the total yield gains over the past 52 weeks to just 37 basis points.

However, the UST 2-year yields fell by a sizable 14 basis points to 3.92% from last Friday’s close of 4.06%. This continues the yield curve inversion between the UST 2-year and 10-year notes into its 43rd consecutive week with the yield spreads narrowing significantly to -48 basis points from -61 basis points last week.

Conversely, the 10-year MGS bond yields also fell by just two (2) basis points to 3.71% from 3.73% last Friday causing the yield spreads between both countries’ 10-year bonds to narrow slightly to 27 basis points from 29 basis points last week.

ECONOMICS

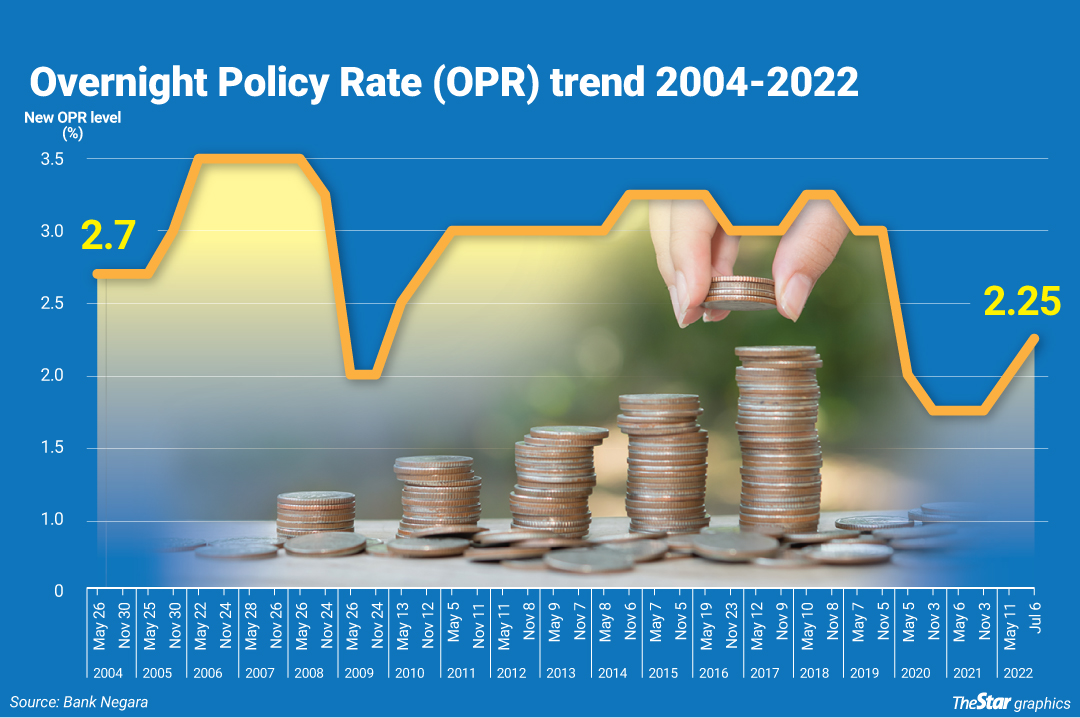

Bank Negara Malaysia (BNM) raised the Overnight Policy Rate (OPR) by 25 basis points (bps) to 3.00% as the central bank believes it is the time to further normalise the degree of monetary accommodation given the continued strength and resiliency in the local economy.

In addition, BNM also recognises the need for an appropriate monetary policy stance that remains consistent with the outlook of domestic inflation and growth to prevent the risk of future financial imbalances.

With the latest rate hike, the ceiling and floor rates of the corridor of the OPR are correspondingly increased to 3.25% and 2.75% respectively. This also brings the OPR back to its pre-Covid-19 level of 3.00%.

The International Air Transport Association (IATA) disclosed that air travel traffic (measured in revenue passenger kilometers) in March 2023 rose by 52.4% year-on-year basis from March 2022.

This was mainly boosted by international air traffic which climbed 68.9% as compared to domestic air traffic which rose 34.1%. So far, international travel has reached 81.6% of pre-COVID-19 levels in March 2019 driven by high demand of Asia Pacific carriers due to China’s lifting of travel restrictions.

CURRENCY

The Ringgit was mixed against the major currencies over the past week despite the surprise OPR rate hike. The local currency gained against the US Dollar at RM4.4350 / USD1.00 (-2.30sen), the British Pound at RM5.5910 / GBP1.00 (-1.20sen) and the Euro at RM4.8920 / EUR1.00 (-2.11sen).

However, it weakened against the Japanese Yen at RM3.30 / JPY100 (+3.00sen) and the Singapore Dollar at RM3.3480 / SGD1.00 (+0.6sen),

MY OPINION

Although the local equities market ended on a higher note for the week, the overall market breadth was negative on last Wednesday and Friday.

Therefore, I believe that the local stock market will be susceptible to a minor sell off in the coming week in the absence of any major positive news flow. I expect the benchmark KLCI to continue consolidating within the 1,400 to 1,450 point range in the coming weeks.

In the US bond markets, the yield movements last week indicates that bond fund managers has started to reflect a normalization of the monetary policy by the US Federal Reserve as they start buying into the shorter end of the yield curve.

However, trouble in the US financial system may re-surface in the near term as news of PacWest Bancorp exploring strategic options (which includes a sale of the bank) hit the market last week. Hence, I expect the bond yields to trade around (+/- 15 basis points) in the coming week.

Going forward, I am maintaining my view that the Ringgit is expected to trade between the RM4.40 - RM4.48 in the coming week.

With all the major monetary policy decisions by the central banks over for the month, the Ringgit is likely to be range bound in the near term. - DagangNews.com

Manokaran Mottain has been an economist with a number of financial institutions and is now managing his own firm, Rising Success Consultancy Sdn Bhd and has been writing his economic analysis on a weekly basis in DagangNews.com since 2022

Layari kami terus di DagangNews.com dan juga

Orang ramai yang ingin memberi pandangan atau suara hati, boleh menghantar tulisan ke [email protected] dengan menyatakan:

1. Nama Pena (Jika tidak mahu guna nama sebenar).

2. Nama Sebenar seperti dalam Kad Pengenalan (Untuk rekod kami).

3. No. Telefon (untuk kami hubungi semula).

4. Menulis mengikut 5 Prinsip Rukun Negara.

5. Tidak melebihi 1,000 patah perkataan.

6. Editor berhak untuk menyunting atau menolak artikel secara profesional.