KUALA LUMPUR 6 July - Tenaga Nasional Berhad (TNB) might see its market price to remain unchanged at RM14 after relatively driven by surcharge removal that further improves the public perception.

Maybank Investment Bank Research (Maybank IB) report continues to expect an eventual re-rating of share price to levels that better reflect TNB’s earnings stability.

TNB also offers a relatively decent recurring dividend yield of c.5% which reflects its recent highest record of dividend at RM RM5.69 billion for 2019 financial.

“We like TNB for its relative earnings stability (regulated revenue is largely fixed, while generation profit is dependent on plant availability, not generation),” said Maybank IB.

However, Maybank IB reiterates the forecast might change due to few factors.

“The Regulatory developments, such as the determination of regulated returns, have a direct impact on earnings. Adverse changes in electricity demand patterns or plant outages could also result in earnings losses for TNB,” said the organisation.

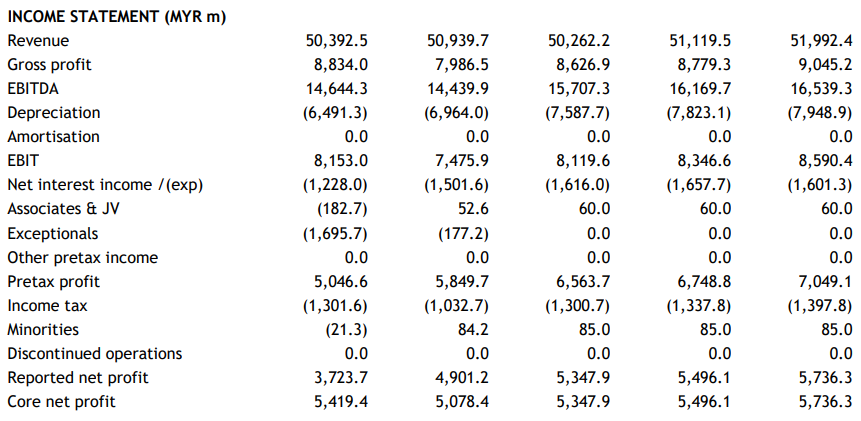

Meanwhile, TNB’s financial year 2020 earnings might set to RM 50,262.2 million with the core net profit of RM5,347.9 million which is higher than 2019’s at RM5,078.4 million and the expected revenue growth of 1.3%.

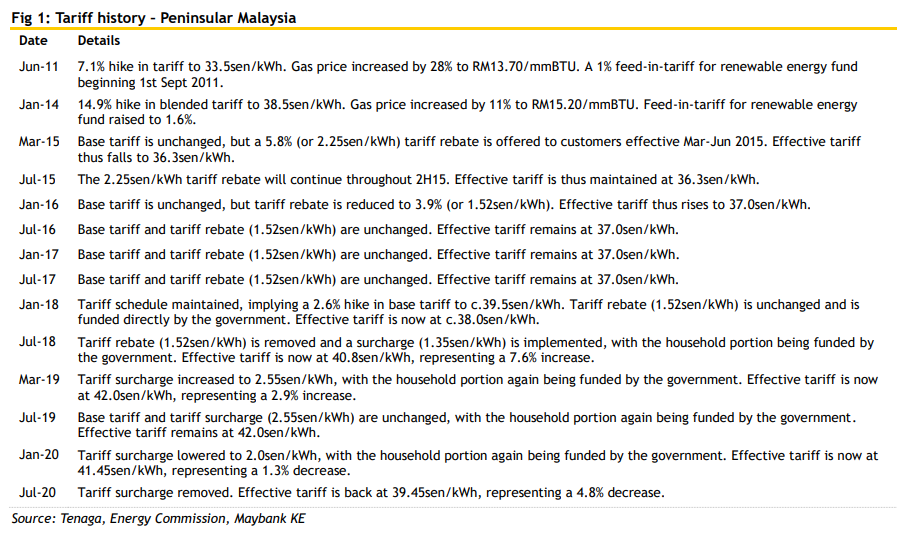

TNB recently removed its tariff surcharge consistent with low coal prices. Lower tariffs should help improve public perception, thus reducing the likelihood of further discounts.

Net tariff is thus slated to fall by 4.8% to 39.45sen/kWh beginning July 2020.

Maybank IB therefore does not rule out another reduction in net tariff in the first half of 2021 as coal prices having fallen further in recent months. - DagangNews.com

Layari kami terus di DagangNews.com dan juga

Orang ramai yang ingin memberi pandangan atau suara hati, boleh menghantar tulisan ke [email protected] dengan menyatakan:

1. Nama Pena (Jika tidak mahu guna nama sebenar).

2. Nama Sebenar seperti dalam Kad Pengenalan (Untuk rekod kami).

3. No. Telefon (untuk kami hubungi semula).

4. Menulis mengikut 5 Prinsip Rukun Negara.

5. Tidak melebihi 1,000 patah perkataan.

6. Editor berhak untuk menyunting atau menolak artikel secara profesional.